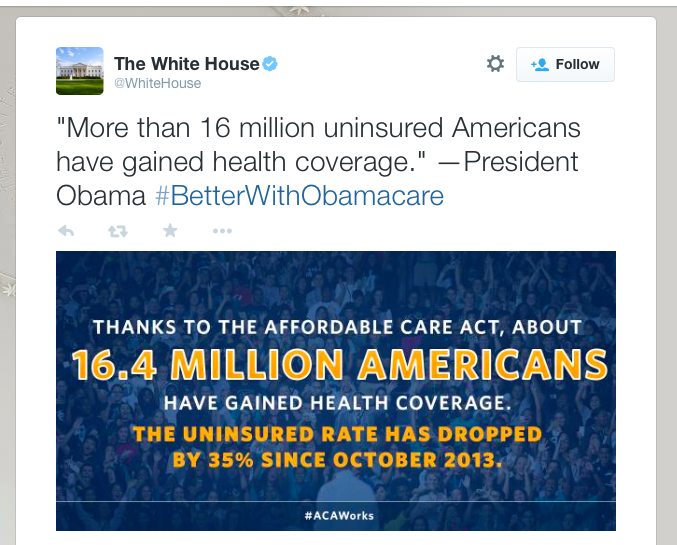

“More than 16 million uninsured Americans have gained health coverage,” Obama recently tweeted, while simultaneously neglecting to mention that this is exactly what you’d expect when you force people to buy insurance.

Force, as I’ve always said, is the heart-and-soul of all (so-called) progressive ideology.

For those who, like me, are being nailed with a “penalty tax” — which, in case you’ve forgotten, is not actually a tax — and likewise for those people who have gotten cancellation notices or have seen premium increases, the news, unfortunately, is not quite so rosy as Obama and his clownish administration would have you believe, all their propaganda to the contrary notwithstanding.

Also, I would be remiss if I didn’t point out the absurdly obvious: namely, forcing people off existing plans in order to force them into more expensive (and inferior) plans does not, to any sane person, constitute success. In fact, that sort of thing only occurs in the minds of bureaucrats and all other similarly insane people.

Here’s what Barack Obama’s tweet actually translates to:

“Forcing people into my bureaucratic nightmare worked even better than I thought it would” (Barack Obama, March 25th, 2015).

Which is, of course, to say nothing of the fact that health “insurance” — i.e. pre-paid healthcare — is the primary reason healthcare is so wildly expensive in America today.

If there’s anyone out there who truly believes Obamacare is a good thing, ask yourself:

Which plan is Obama and his family on?

Ask yourself further:

If Obamacare is so excellent, why are Democratic Senators begging for another delay?

Prediction: we’ll only hear crickets chirping in response to my challenge for anyone — anyone — to defend to me this bureaucratic monstrosity known as Obamacare. And the reason we’ll only hear crickets chirping is that anyone who attempts to defend this will, in effect, be defending the wild notion that the IRS has and should have legitimate control over your health.

“If you like your plan, you can keep your plan. Period.” — Barack Obama, 2009, 2010, 2011, 2012, 2013.

The dynamic Doctor Mariela Resendes (M.D.) is a private practitioner who spent her previous 5 years as the Managing Partner/CEO of the largest Radiology practice in the San Joaquin Valley of California, CMI Radiology Group. Just recently, she wrote an irrefutable and scathing essay on the coming healthcare disaster that Barack Obama and his clownish administration have just unleashed. I reprint it here in full:

As a practicing doctor in California it troubles me that those with the ability to influence health care legislation have either been politically motivated to remain silent, or strikingly inarticulate when it comes to voicing the major issues patients and taxpayers will face with the new health care bill. My own, long-held view has been that any reform should be of the free market variety.

In that sense, I’m increasingly scared as I learn more about what’s inside the health legislation passed by Congress not long ago. Despite the rising level of unhappiness with what has transpired, it dismays me that the general public, like me, is not fully aware of the financial tsunami that is on the way for patients, insurers and hospitals thanks to this legislation, not to mention the irregular way in which it was passed.

In the newspapers we all read that the legislation was passed via reconciliation. Most people do not understand what this represented. What Congress did was to pass this legislation under the Congressional Budget Act of 1984, which allows a loophole to avoid a 60 vote filibuster in laws which refer to changes in revenue and spending amounts; i.e. budgetary issues.

The legislation which Congress passed certainly does affect the budget, but clearly the bill’s intent wasn’t budgetary; rather it concerned dramatic changes for a large portion of our economy: health care. Given the bill’s intent, one can only hope that the upcoming elections bring greater ideological balance so that what promises to be damaging can at the very least be amended.

“Obamacare”, as it is colloquially termed, is financially a disaster for doctors, hospitals, insurers, and will ultimately be a disaster for our nation’s budget. It is also unfortunate for patients needing care.

Obamacare’s proponents tout the legislation’s cost controls, along with expansion of coverage for those who currently do not have insurance. The policy wonks seek cost containment and “efficient” use of resources. More realistically, cost containment could only be achieved if access to care were rationed.

Rationing in mind, Rahm Emmanuel’s brother published a very well received paper in the New England Journal Of Medicine about efficient or optimal deployment of resources in health care. The upshot is that a young man is worth spending a lot of money on, a young child much less, and for seniors, pretty much nothing; all in a calculated return on investment model.

For physicians, Obamacare initially offered promises of tort reform, as well as promises to reverse the Medicare cuts that made it so difficult for physicians to practice. Neither is in the final legislation. As a result, doctors will continue to practice defensive medicine, and for doing so will face 20%+ cuts in their Medicare payments.

Physicians in primary care will initially see an income boost from 2011-2014, thus encouraging them to take on indigent patients the system needs to absorb. Unfortunately, starting in 2014, the payments per patient will fall for primary care doctors too.

Specialists will receive a financial hit right from the beginning. The goal here is to have less in the way of specialists, and more general practitioners. On its face this will drive more doctors into early retirement.

As for the physicians that choose to continue practicing, they’ll have difficulty staying afloat financially, and many will seek employment opportunities similar to those of “foundation” practices (such as those seen in states like California where hospitals can’t employ physicians), or hospital owned practices in other states.

The explicit goal here is to slow the move toward private practice. Doctors in foundation types of practices act more like union or shift-workers, and less like professionals. Their productivity tends to be lower than in traditional private practices; ergo more doctors are needed for a similar number of patients. Considering a scenario of rising physician retirement alongside a large increase in the number of patients, it is unclear how treatment and diagnosis will occur in a timely fashion.

Hospitals are similarly not going to fare well, and many will simply go under. Previously, hospitals took in higher payments from privately insured patients in order to care for those who couldn’t pay, or for those covered by Medicaid. At the same time, hospitals which had a higher number of indigent patients also received what is called disproportionate share funds from state and federal governments. Rural hospitals in particular received extra funds.

But with Washington’s new mandate, the expectation is that all of the previous non-paying patients will now pay for themselves such that subsidies for indigent-care will be eliminated. Unfortunately, this will occur in concert with reduced inflows from privately insured patients whose costs will be reduced to Medicaid levels.

In short, the money from the increased volume of “paying” patients is not enough to counter the loss of disproportionate funds and decreased classic private insurance payments. The net result will be a deficit for many hospitals. They will not be able to keep their doors open if they sustain persistent losses, which is what is expected.

Many insurance companies will be squeezed out of existence thanks to rules that will bar them from denying coverage for pre-existing conditions. And unlike the federal government they won’t be able to operate in the red forever. The end result points to a single-payer system run out of Washington.

Looking ahead, it is increasingly apparent that by 2020 we will have severe cuts in service thanks to rising retirement among doctors, a decrease in the number of private insurers, and a reduction in the number of hospitals due to federal mandates that fail to marry costs with services. The end result will be rationing and delay of elective procedures, denial of expensive but effective treatments a la England, and most likely a single-payer system the likes of which is seen in other, less advanced health care systems around the world.

What is now termed modern medicine actually began in the early 1920s when science — in particular, germ theory — culminated to a point that sickness and disease were at last being treated reliably.

It was then that doctors and hospitals got much better at the business of saving lives. This more highly developed service and expertise raised the value of their work, and they charged accordingly for their increased skill and labor.

And that, really, is when the situation started: when lives can be saved and health can be gained because of developments in technology, everyone suddenly believes that it’s his or her right to have that thing.

We see the same principle at work in, for example, the platitude “No one should go hungry when Americans are throwing away food.”

The error in both cases is the fraudulent notion that survival should be assured. This notion neglects the singular fact that abundance and technology are produced — and produced, moreover, by individuals.

No one has the right to the life and labor (i.e. production) of any individual, including the life and labor of doctors.

An easy way to demonstrate this truth is by asking the following: where was that right before these goods and services were produced or invented?

It is a fact that American medicine is already 50 percent socialized.

It is also a fact that there’s a clear correlation between rising healthcare costs and the socialization of medicine in this country. More government intervention will only compound the problem.

In the 1920s, when advancing healthcare became more expensive (though still very reasonable), the administrator of Baylor Hospital in Dallas, one Dr. Justin Ford Kimball, created a system called Blue Cross. The Blues (so-called) were nonprofit health insurers. They served local organizations like the Rebeccas and the Elks Club, and — please pay attention — they kept their premiums low in exchange for tax breaks.

Tax breaks are one of the main components to our current healthcare crisis. They’re what initially created the problem.

Blue Cross, you see, was successful only because of these tax breaks. Up until then, commercial insurers had always regarded medicine as a mediocre market, and therefore commercial insurers didn’t deal too much in medicine. But when commercial insurers saw that the Blues were making money, it convinced them to enter the medical field. This was not a problem, at first — until the 1940s, when private insurers increased their efforts to get around wartime wage controls, thus:

During World War II, Franklin Delano Roosevelt’s price-and-wage people, who didn’t generally permit wage increases or price increases (regardless of market forces) sanctioned a form of tax discrimination: specifically, they allowed employers to pay for employee medical insurance with pretax dollars.

This quickly became one of the few ways employers could attract new and better employees, since FDR had actually mandated that employers were no longer permitted to pay out higher wages. (How this ridiculous idea came about is another story, for another time.)

To this day, those who get employer-financed healthcare are purchasing their healthcare coverage with pretax dollars. On the other hand, those who buy their own healthcare are purchasing it with after-tax dollars.

This is a much bigger issue than you might at first realize.

As far as the employer was (initially) concerned, this wasn’t any different from additional labor costs — which is to say, medical insurance was not, from the employers perspective, any different from a rise in wages, and yet FDR’s price-and-wage control people did not at all see it as a wage increase. They therefore allowed it, which may seem surprising in light of FDR’s desire to control the entire economy.

Likewise, the IRS bureaucrats under FDR did not regard this maneuver as a wage increase, and for this reason they didn’t slap a tax on it. Neither did the employees see it as a real raise in wages — a fact that is singular to how this whole horrible precedent was set — because these costs are what economists call hidden costs.

The upshot: people didn’t and very often still don’t know that it is, after all, their own money paying for this prepaid medical coverage, and that medical coverage isn’t free.

In fact, health insurance today isn’t even really health insurance. It’s more properly called prepaid healthcare. But — and this is an another crux — it gives the appearance of being free or substantially free to the user, and it therefore substantially increases the demand for it and therefore its cost.

Of course, the root of this whole problem is the misbegotten notion that healthcare is not a good and service to be traded on the open market, but a right.

Let us remember what insurance actually is:

Insurance, properly defined, is what you purchase in order to avoid financial ruin in the case of a rare emergency.

Under the dangerous system FDR created, employees came to regard their healthcare coverage as a kind of blessed phenomena which came without cause or consequence. Quickly, this phenomena was absorbed into the working culture and as quickly was taken for granted: employees got used to receiving free goods, which goods, however, were not actually free. Employees just could not see that they were paying for them, and paying for them, furthermore, with pretax dollars.

A family in the bottom fifth of the income distribution pays about $450 more in taxes than insured families at the same income level. For families in the top fifth of the income distribution, the tax penalty is $1,780. On average, uninsured families pay about $1,018 more in federal taxes each year because they do not have employer-provided insurance. Collectively, the uninsured pay about $17.1 billion in extra taxes each year because they do not receive the same tax break as insured people with similar income. If state and local taxes are included, the extra taxes paid by the uninsured exceed $19 billion per year (“Are the uninsured freeloaders?” National Center for Policy Analysis, Brief Analysis No. 120).

Among other things, this illustrates again why entitlements are such a deadly precedent: once they’re entrenched, it’s virtually impossible to retrogress. Why? Because people acclimate to entitlements and in no time cannot imagine life without them.